27 E Trevor Rd, Colbert, WA is officially closed! I’m grateful for the opportunity to have represented my client in this successful transaction. Every closing is more than just a sale—it’s a step forward in someone’s journey, and I’m honored to be part of it. If you’re thinking about buying, selling, or investing in real estate, I’m here to guide you every step of the way. Let’s make your next move a success. – Christopher Odinde

Buy and Hold

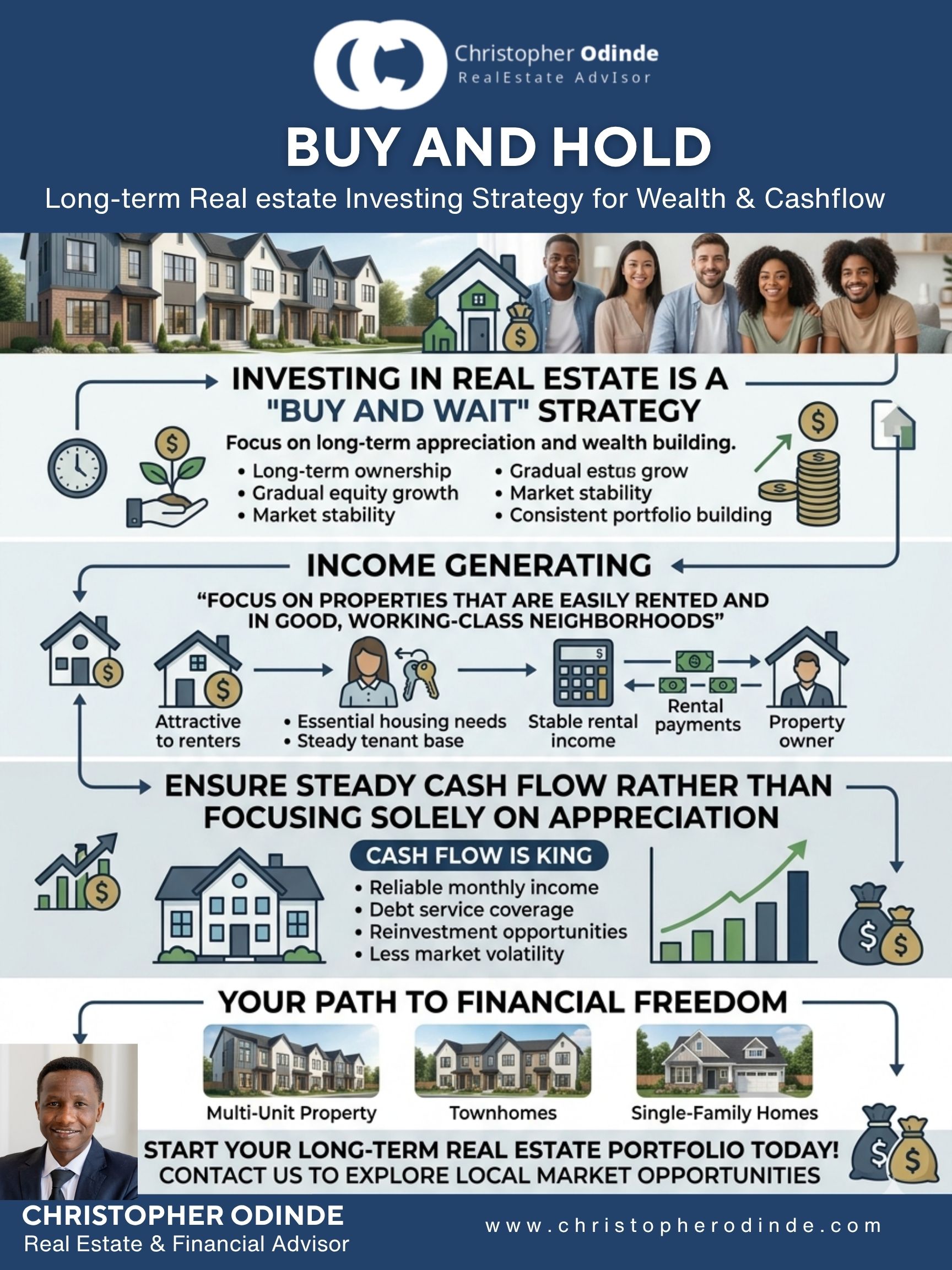

1: The “Focus on Cash Flow” Approach (Best for LinkedIn or Instagram) Caption: Forget the speculation and the stressful hunt for the next “hot” neighborhood. The real secret to long-term real estate wealth isn’t hitting a home run on appreciation—it’s consistent, reliable cash flow. The “Buy and Hold” strategy, often called “Buy and Wait,” is the foundation of institutional investing. The goal is simple: Acquire properties in solid, working-class neighborhoods where people always need quality housing. By focusing on high-demand, easily rented units, you generate steady income that covers your costs and builds equity now, rather than relying on a potential payout years down the road. It’s about building a portfolio that works for you every single month. Ready to shift your focus from appreciation to immediate income? Let’s connect to explore steady-income opportunities in our local market. 2: The “Wealth and Stability” Approach (Short and Punchy for Instagram) Caption: Real estate investing isn’t about being fast; it’s about being right. The “Buy and Wait” strategy (or Buy and Hold) is a powerful, low-volatility path to true wealth. By focusing on cash-flow properties in strong, working-class communities, you build a resilient portfolio. You get: ✅ Steady, reliable income every month. ✅ Equity growth (while your tenants pay the mortgage). ✅ A hedge against market volatility. Prioritize monthly cash flow over future appreciation. It’s the difference between investing and speculating. DM us to see how we identify high-yield, stable properties that make sense from Day 1. 3: The “Professional/Analytical” Approach (Best for LinkedIn) Caption: A strong real estate investment portfolio requires a foundational “Buy and Hold” strategy. While market appreciation is a valuable bonus, focusing solely on it introduces significant risk. The key to long-term portfolio stability is prioritizing steady, repeatable cash flow. By acquiring properties that are easily rented—specifically in good, working-class neighborhoods—investors can secure immediate income and mitigate market volatility. This “Buy and Wait” approach treats real estate like a income-generating business, not a speculative bet. It ensures a consistent income stream while equity and long-term appreciation are built over time. For an analytical look at the cash-flow potential in our current market, or to discuss how this strategy fits into your portfolio, please reach out directly.

By wisdom a house is built”

God gives wisdom and revelation for the wealth-building methods that are best for each individual. Psalm 127:1 (ESV) says: “Unless the Lord builds the house, those who build it labor in vain.” I remember the exact moment when the lightbulb went off in my head. In my younger years, I was the head of an organization that hosted a major conference. By major, I mean that there were several private jets on the runway! When the conference was over, two of the guys who flew on their own planes joined me in the Colorado hot springs for some rest and relaxation. As we stood in the hot water, one of the men said something that alarmed me greatly. “Billy, if I didn’t have my job, I’d be broke in 90 days. I would literally be out on the street.” I was shocked because this man– a man who flew in on his company’s private jet– was someone I aspired to be like professionally. I realized that people needed a better way to sustain wealth for themselves and others— including me. Shortly after that, I dove deeper into real estate investing. If you’re reading this, chances are that you are seeking God’s wisdom on how to metaphorically build a house (or houses) through real estate investing. God is no respecter of persons. What He does for someone, He’ll do for another. If He can do it for Becky and me, He can do it for you! “And by understanding it is established;” Understanding comes by doing. You must get in the game of real estate and apply these teachings if you want to acquire understanding. Waiting too long to invest is one of the biggest mistakes I see people make in real estate investing. If you start sooner rather than later, you are able to increase your wealth even more because you will gain more assets, get the benefit of income, as well as the growth and appreciation of those assets. The Rule of 72 states that at 20 percent interest, your money would double every five years. So, the sooner you get involved, the better—the longer you hold your assets, the more your net worth and income stream can grow. ‘Established’ is defined as achieving permanent acceptance or recognition. Properties aren’t just buildings anymore— they are established. Whether you live in them, you share them with loved ones, or you rent them out, they can be vessels for sharing the love of God through growing fellowship and finances. “By knowledge the rooms are filled with all precious and pleasant riches.” That’s a nice image, isn’t it? Rooms full of decor, color, and value. The continual pursuit of knowledge is the KEY to sustainable wealth. Proverbs 15:22 (NKJV) says “Without counsel, plans go awry, but in the multitude of counselors they are established.” You must ask questions and build connections! A big mistake I see newcomers make is not obtaining a professional opinion on everything— especially property values. When you receive information, name sure that you verify and get everything in writing. If it’s not in writing, it doesn’t count. Another way to gain knowledge is through investing in the resources on our site, as well as pre-ordering my new book ‘Strategic Real Estate Investing’ (on sale for a limited time). And, be on the lookout for information on our Real Estate Investment Workshop coming in March!

Future of Real Estate

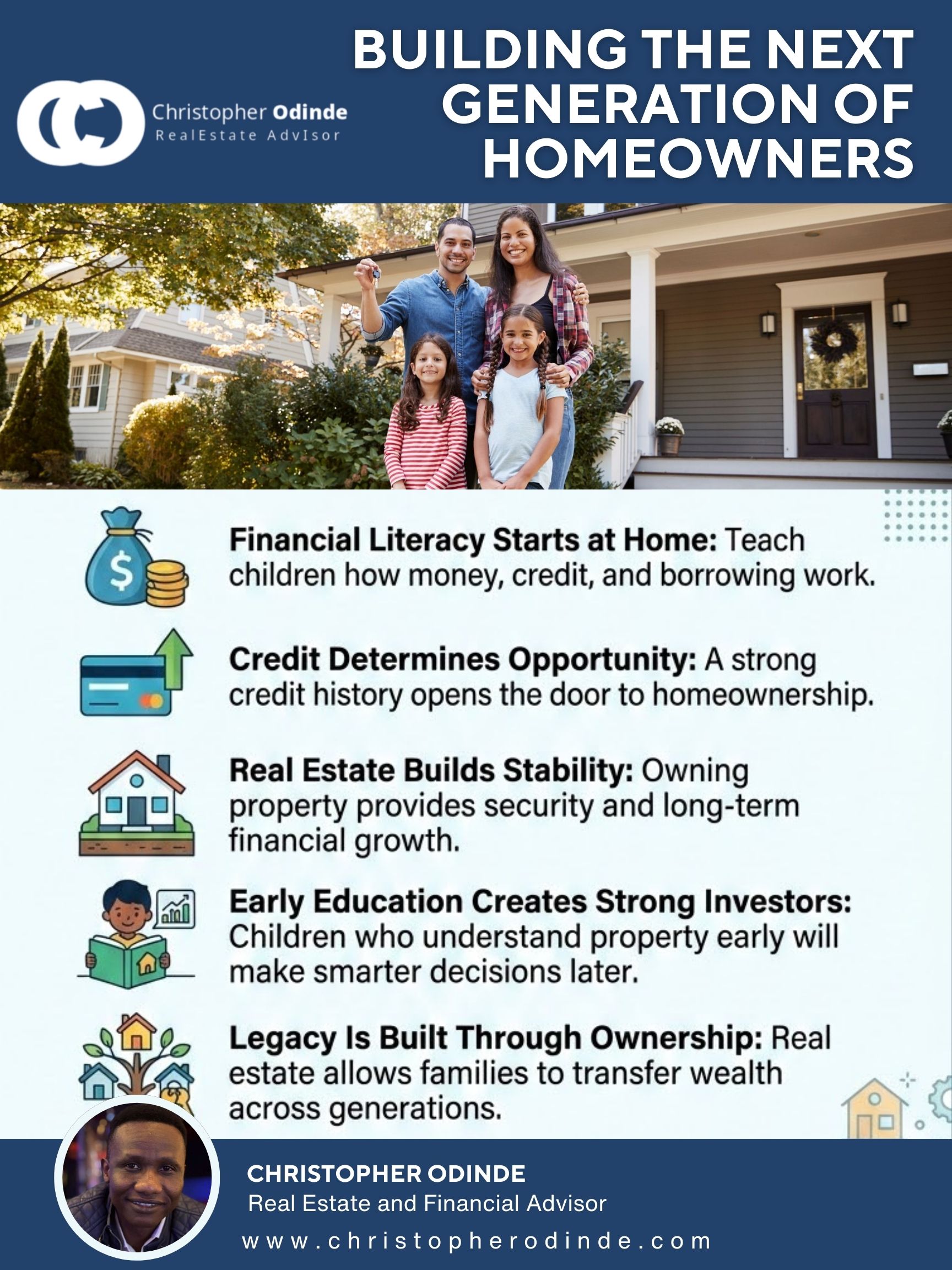

The Future of Real estate The Future of Real Estate Depends on Financial Intelligence and Intentional Living The real estate industry is evolving. Markets shift, interest rates fluctuate, and economic conditions change—but one truth remains constant: The future of real estate is not determined by the market alone. It is shaped by the knowledge, discipline, and financial awareness of those who participate in it. For individuals and families seeking long-term stability and wealth, real estate is more than a transaction—it is a strategy. And that strategy is built on five key pillars. 1. Financial Literacy: The Foundation of Every Decision At the core of every successful real estate journey is a strong understanding of personal finance. Financial literacy is not just about earning money—it is about: Managing cash flow Controlling expenses Planning for long-term goals Making informed financial decisions Without this foundation, even the best real estate opportunities can become financial burdens instead of assets. When individuals learn to organize their finances effectively, they position themselves to enter the real estate market with confidence and clarity. 2. Creditworthiness: Your Financial Reputation In today’s economy, your credit profile is one of your most powerful financial tools. Creditworthiness reflects: Your reliability as a borrower Your financial discipline Your ability to access opportunities More importantly, credit is not just something to maintain—it is something to use strategically. When used wisely, credit becomes a lever that allows you to acquire appreciating assets, including real estate. Many pathways to homeownership are supported by institutions such as the Federal Housing Administration and programs connected to the U.S. Department of Veterans Affairs, making it possible for qualified buyers to enter the market with structured financing options. Understanding how to build and use credit effectively is a defining factor in long-term success. 3. Real Estate Investment Knowledge: Understanding the Game Real estate is one of the most powerful wealth-building tools—but only for those who understand how it works. Key principles include: Location — the driving force behind property value Appreciation — how property values grow over time Leverage — using borrowed capital to increase potential returns Without this knowledge, buyers may make decisions based on emotion rather than strategy. With it, they can evaluate opportunities, minimize risk, and maximize long-term value. 4. Educating the Next Generation The future of real estate does not stop with one purchase—it extends to the next generation. One of the most overlooked aspects of wealth building is financial education within the family. Teaching children about: Money management Credit Investing Homeownership …creates a cycle of knowledge and opportunity that can last for generations. Families that prioritize education around real estate and finance are not just building wealth—they are building legacy systems. 5. Legacy and Wealth Transfer: Thinking Beyond Today True wealth is not just what you build—it is what you preserve and pass on. Legacy planning involves: Structuring assets effectively Protecting wealth from unnecessary loss Ensuring smooth transfer to future generations Real estate plays a critical role in this process because it is a tangible, enduring asset that can provide both income and long-term value. Those who think beyond immediate gains and plan for generational impact position themselves differently. They move from short-term success to lasting influence. Final Thoughts: Building the Future Intentionally The future of real estate will belong to those who approach it with intention, education, and strategy. It is not about timing the market perfectly.It is about preparing yourself to act when opportunities arise. When you combine: Financial literacy Strong credit Investment knowledge Family education And legacy planning You create more than just ownership—you create a framework for generational wealth.

Grace-motivated Service

Grace-motivated Service 1 peter 4:10 service “Each of you should use whatever gift you have received to serve others, as faithful stewards of God’s grace in its various forms.” Our whole purpose as your real estate and financial planner is to serve you and your family. We continually strive to learn and grow to stay ahead of the industry, and to have the greatest ability to serve you well. Through grace-motivated service we actively pursue putting your needs and best interests first, and we take delight in meeting those needs. A relationship built on service is a relationship destined to thrive. We would love to establish deeper fellowship with you and your loved ones so we can learn how to best serve you over the long haul. As we grow together, we plan to add experienced and like-minded members to our team to maintain a high level of service.

Real Estate Portfolio

Real Estate Portfolio Ready to Build Your Real Estate Portfolio? Let’s Talk. We’ve all heard the stories: the “accidental landlord” who turned a spare condo into a goldmine, or the mogul who started with one duplex and now owns half the block. It sounds like the dream, right? Passive income, tax breaks, and a tangible asset that grows while you sleep. But if you’re standing on the sidelines, the gap between “I want to invest” and “I just closed on my third property” can feel like a canyon. Estate Portfolio We’ve all heard the stories: the “accidental landlord” who turned a spare condo into a goldmine, or the mogul who started with one duplex and now owns half the block. It sounds like the dream, right? Passive income, tax breaks, and a tangible asset that grows while you sleep. But if you’re standing on the sidelines, the gap between “I want to invest” and “I just closed on my third property” can feel like a canyon. The truth? Building a portfolio isn’t about having millions in the bank—it’s about having a strategy. If you’re ready to stop dreaming and start scaling, here is how we get the ball rolling. 1. Define Your “Why” (and Your “How”) Before you look at a single listing, you need to know what kind of investor you want to be. Are you chasing cash flow (monthly profit) or appreciation (long-term wealth)? The Buy-and-Hold: Classic rental properties. Reliable, steady, and great for long-term wealth. The BRRRR Method: Buy, Rehab, Rent, Refinance, Repeat. This is the “fast track” for those willing to get their hands dirty. Short-Term Rentals: Airbnbs and vacation spots. Higher management intensity, but often higher yields. 2. The Power of “Leads” Over “Listings” By the time a property hits a major real estate site, the competition is fierce. Building a true portfolio requires finding value where others don’t. This means looking for: Off-market deals. Distressed properties with “good bones.” Emerging neighborhoods just outside the current “hot spots.” 3. Treat It Like a Business, Not a Hobby A portfolio isn’t just a collection of houses; it’s a business entity. To scale successfully, you need your “Board of Directors” in place: A Savvy Lender: Someone who understands investor-specific loans (like DSCR loans). A Rock-Star Property Manager: Because “passive” income shouldn’t mean a 2:00 AM phone call about a leaky toilet. A Trusted Contractor: To keep your margins tight and your finishes sharp. The Reality Check Real estate is a marathon, not a sprint. You might start with a modest $200,000 condo, but through the power of equity and leverage, that one unit can become five in a few short years. Pro Tip: Don’t wait to buy real estate. Buy real estate and wait. Let’s Get Practical If you’ve been waiting for a “sign” to start your investment journey, this is it. But you shouldn’t go it alone. Whether you’re looking for your first rental or your tenth, the right move depends on current market data and your specific financial goals.

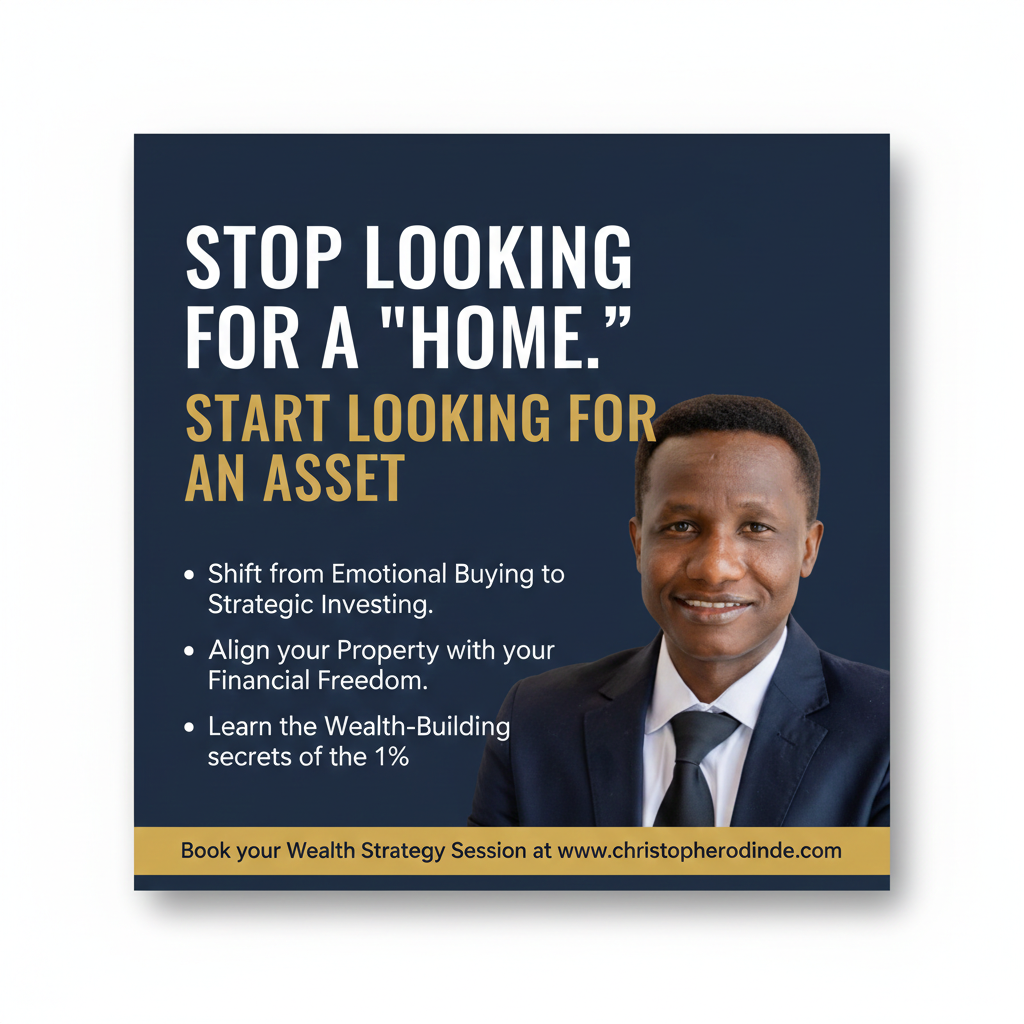

Stop Buying a ‘Home’ and Start Acquiring Assets

Beyond the Front Door The Emotional Trap of the “Dream Home” When you look for a home, you’re looking through an emotional lens. You’re thinking about the color of the walls, the size of the backyard for the kids, or how close it is to your favorite coffee shop. While these things are important for your quality of life, they often cloud your judgment of the property’s financial performance. When you buy emotionally, you are more likely to: Overpay because you “fell in love” with the house. Over-improve the property with luxury finishes that won’t yield a return on investment. Ignore market data in favor of personal convenience. Why You Need to Stop Buying a ‘Home’ and Start Acquiring Assets For most people, buying a home is the single largest financial transaction of their lives. It’s a milestone often celebrated with champagne and a set of shiny new keys. But as a Wealth Coach and Financial Advisor, I’m going to tell you something that might surprise you: Your dream home is often your biggest financial liability. If you want to build true, generational wealth, you need to shift your mindset. You need to stop looking for a “home” and start looking for an asset. What Does it Mean to Buy an “Asset”? An asset, by definition, is something that puts money into your pocket. A liability is something that takes money out. When I advise my clients to look for an asset, we focus on three specific financial pillars: 1. The Numbers Over the Neighborhood An asset is chosen based on its Capitalization Rate (Cap Rate) and cash flow potential. If you were to move out tomorrow, would the rent cover the mortgage, taxes, insurance, and maintenance? If the answer is no, you haven’t bought an asset; you’ve bought a high-priced hobby. 2. Forced Equity and Appreciation A “home” owner waits for the market to go up. An investor looks for ways to force the value up. Whether it’s adding a secondary suite, optimizing the layout, or buying in a path of planned urban development, an asset-first approach focuses on growth that you can control. 3. The Tax Shield As a Financial Advisor, I help clients see the hidden “income” in real estate. From depreciation to interest deductions, an asset provides tax advantages that a simple primary residence often cannot match. How to Make the Shift You don’t have to live in a warehouse to be an investor. You can still live in a beautiful house—but you should purchase it with an investor’s exit strategy. Ask yourself: “If the market drops 10% tomorrow, how does this property protect my net worth?” Analyze the ‘Highest and Best Use’: Is this property a single-family home today but a potential multi-family lot tomorrow? Building Your Wealth Strategy Real estate is the most proven vehicle for building wealth, but only if it’s driven by a strategy, not a dream. My mission as your Wealth Coach is to ensure that every door you unlock is a door to financial freedom. Ready to stop “housing” your money and start growing it? Let’s look at your portfolio through a different lens. Visit me at www.christopherodinde.com to book a strategy session.

The Ultimate Guide for home-buyers

The Ultimate Homeownership Guide Many people dream of owning a home, but the process of making that goal a reality may be quite difficult. You can find a property you love that fits your budget and navigate the homebuying process with confidence if you have the proper advice and are prepared. We will walk you through every step of the homebuying process in this guide so you can be ready to make informed choices. We will go over everything you need to know, from examining your financing possibilities to closing on your new house. Here’s to making your homeownership dreams come true. Book Description The Ultimate Guide for Homebuyers: Everything You Need to Know Before You Buy Your Home is a practical, easy-to-understand roadmap designed to help buyers navigate the homeownership journey with clarity and confidence. From preparing your finances and understanding credit, to choosing the right loan, making a strong offer, and successfully closing on a home, this book breaks down the entire process step by step. It addresses common myths, costly mistakes, and overlooked details that often confuse first-time buyers and even experienced homeowners. Whether you are buying your very first home or planning your next property as a strategic investment, this guide equips you with the knowledge, tools, and mindset needed to make smart decisions that lead to long-term stability and wealth through real estate. About the Author Christopher Odinde is a real estate professional, investor, and educator with a passion for helping individuals and families achieve confident and sustainable homeownership. With a background in technology, business, and real estate, Christopher brings a unique, strategic approach to buying and owning property. Having worked closely with first-time buyers, immigrants, and investors, he understands the real challenges people face when entering the housing market. His mission is to simplify real estate, empower buyers with knowledge, and help communities build wealth through informed homeownership decisions. Through his work, Christopher combines practical experience, financial insight, and a heart for service—guiding readers beyond just buying a home, toward building a lasting legacy. Download Your Copy

Buying a home

Getting ready to buy a home Determine Your Budget The first step in buying a home is to establish a clear budget. This involves assessing your financial situation, including your income, savings, and existing debts. Mortgage lenders typically consider your debt-to-income ratio, which compares your monthly debt payments to your gross monthly income. In addition to the purchase price, you should also factor in costs like property taxes, homeowner’s insurance, maintenance, and any homeowners association (HOA) fees. Understanding your financial capacity will help you narrow down your home search and avoid overextending yourself. Get Pre-Approved for a Mortgage Once you have a budget in mind, the next step is to get pre-approved for a mortgage. This is a process where a lender evaluates your financial background and creditworthiness to determine how much they are willing to lend you. A pre-approval letter not only gives you a clearer picture of your price range but also strengthens your position as a buyer. It shows sellers that you are serious and capable of securing financing, which can be a significant advantage in a competitive market. Choose a Location Selecting the right location is just as important as choosing the right home. Consider factors such as the quality of local schools, accessibility to public transportation, proximity to your workplace, and the availability of nearby amenities like grocery stores, parks, and recreational facilities. You might also want to look into safety ratings and the general vibe of the neighborhood. Researching potential developments in the area can also provide insight into future growth that may affect property values. Find a Real Estate Agent Having a knowledgeable real estate agent can make a significant difference in your home-buying experience. An agent can help you navigate the complexities of the real estate market, offering access to listings that match your criteria and helping you stay informed about market trends. They also facilitate communication with sellers and other stakeholders, ensuring that you are well-represented throughout the process. When selecting an agent, look for one with good reviews and a solid track record in your preferred neighborhoods. Start House Hunting With your budget established, pre-approval in hand, and an agent on your side, it’s time to start house hunting. Create a list of must-haves and nice-to-haves to guide your search. Attend open houses to get a feel for different properties, and don’t hesitate to ask your agent for private showings of homes that catch your eye. Take notes during your viewings to help you remember details about each property, as it can be overwhelming to keep track of multiple homes. Make an Offer When you find a home that meets your needs, the next step is to make a formal offer. Your real estate agent will help you formulate an offer that reflects the home’s market value and the current conditions. They will also explain contingencies that can protect you, such as financing and inspection contingencies. Once both parties agree, your offer will enter into a negotiation phase, where you may need to go back and forth until reaching mutually agreeable terms. Home Inspection After your offer is accepted, it’s crucial to conduct a home inspection. This step allows you to identify any potential issues with the property before finalizing your purchase. A qualified home inspector will evaluate the home’s condition, including structural aspects, electrical systems, plumbing, and HVAC systems. Based on the findings, you may negotiate repairs or credits with the seller or, in some cases, decide to withdraw your offer if the issues are extensive. Finalize Financing After the inspection, you’ll finish securing your mortgage. This task involves working closely with your lender to finalize the loan terms, complete any required paperwork, and provide additional documentation as needed. Ensure that you understand the interest rates, terms, and any fees associated with your mortgage. It’s an important step that sets the stage for the closing process. Closing The closing is the final step in the home-buying process, where ownership is officially transferred. During this meeting, you’ll review and sign various legal documents, including the mortgage agreement and title transfer documents. Be prepared to pay closing costs, which may include loan origination fees, appraisal fees, and title insurance. After the paperwork is completed and funds are disbursed, you will receive the keys to your new home! Move In Once the sale is finalized, you can make arrangements to move into your new home. It’s a time filled with excitement as you begin to personalize your space. Planning your move efficiently—whether hiring movers or enlisting friends—can help reduce stress. Take your time settling in and exploring your new neighborhood, making sure to establish utilities and address any immediate needs for your new home. If you have specific questions about any of these steps or need further information, feel free to contact me!

Landlords Make Wealth in Their Sleep

Here’s Why Most people trade time for money. They wake up, go to work, and earn a paycheck that stops the moment they stop working. Landlords, however, build systems that generate income whether they are awake or asleep. This is not luck, and it is not magic—it is the result of owning assets that produce cash flow, grow in value, and benefit from time itself. At the heart of a landlord’s wealth is recurring rental income. Each month, tenants pay rent, and that rent covers expenses such as the mortgage, taxes, insurance, and maintenance. Over time, what remains becomes predictable cash flow. Unlike wages that depend on constant labor, rental income continues as long as the property is well managed and in demand. This steady flow of income creates financial stability and frees landlords from living paycheck to paycheck. Another powerful advantage landlords enjoy is appreciation. Real estate tends to increase in value over the long term due to population growth, limited land supply, inflation, and economic development. While owners go about their daily lives, their properties quietly grow in value. This means a landlord can become significantly wealthier on paper without actively doing anything, simply by holding the asset over time. Landlords also understand leverage—using other people’s money to build wealth. By using credit responsibly, they control valuable properties with relatively small down payments. Tenants then help pay down the mortgage, effectively buying the property for the landlord over time. When used wisely, credit stops being a burden and becomes a tool for expansion and wealth creation. The tax system further rewards property owners. Landlords can deduct expenses related to maintaining and operating their properties, and they benefit from depreciation, a non-cash expense that reduces taxable income. While employees often pay taxes first and live on what remains, landlords structure their finances so they legally reduce taxes and reinvest more of their income into growing their portfolio. Inflation, which erodes the purchasing power of cash, works in favor of landlords. As the cost of living rises, rents typically increase, but fixed-rate mortgage payments remain the same. Over time, landlords repay yesterday’s debt with today’s inflated dollars, while their income keeps pace with rising prices. This natural hedge against inflation is one of real estate’s most underestimated strengths. Every rent payment also builds equity. As the mortgage balance decreases and the property value rises, landlords accumulate wealth they can access through refinancing or borrowing. This equity can be used to acquire additional properties, allowing wealth to compound. One property can eventually lead to many, all funded by systems rather than constant labor. Perhaps most importantly, landlords focus on systems instead of stress. With professional property managers, automated rent collection, and reliable maintenance teams, real estate can become largely passive. Once the right structures are in place, income continues with minimal day-to-day involvement, making true “sleep-time wealth” possible. In the long run, rental real estate creates generational wealth. Properties do not retire, call in sick, or stop producing income. They can be passed down to children, providing long-term financial security and opportunity. This is how families shift from survival to stability, and from stability to legacy. Landlords do not get rich overnight. They get rich deliberately, patiently, and strategically. By owning assets instead of selling time, they allow money, time, and systems to work together. That is why landlords make wealth in their sleep—and why real estate remains one of the most powerful wealth-building tools ever created.